Navigating Malta’s Double Taxation Treaties for Your International Business

For businesses expanding internationally or managing cross-border investments, one of the most significant financial hurdles can be the spectre of double taxation – the risk of having the same income taxed twice, once in the country where it arises and again in the country of residence. This can severely erode profits and act as a major disincentive to global trade and investment. Fortunately, most developed economies, including Malta, address this through a network of Double Taxation Treaties (DTTs), also known as Double Tax Agreements (DTAs).

Malta boasts an extensive network of over 70 DTTs with various countries worldwide. For businesses considering Malta company formation as a hub for their international operations, understanding how these treaties work in practice and the key benefits they offer is crucial for effective tax planning and financial efficiency. How do DTTs actually prevent double taxation? What types of income do they typically cover? And how can your Maltese company leverage these agreements to reduce withholding taxes on payments received from abroad or to provide certainty on taxing rights?

As corporate services consultants at Contact Advisory Services Ltd., a core part of our advisory for internationally focused clients involves considering the implications of Malta’s DTT network. This guide will explain the fundamental principles of Double Taxation Treaties, how they function in the Maltese context, and the tangible benefits they can bring to your business operating from or through Malta.

What is a Double Taxation Treaty (DTT)? The Core Purpose

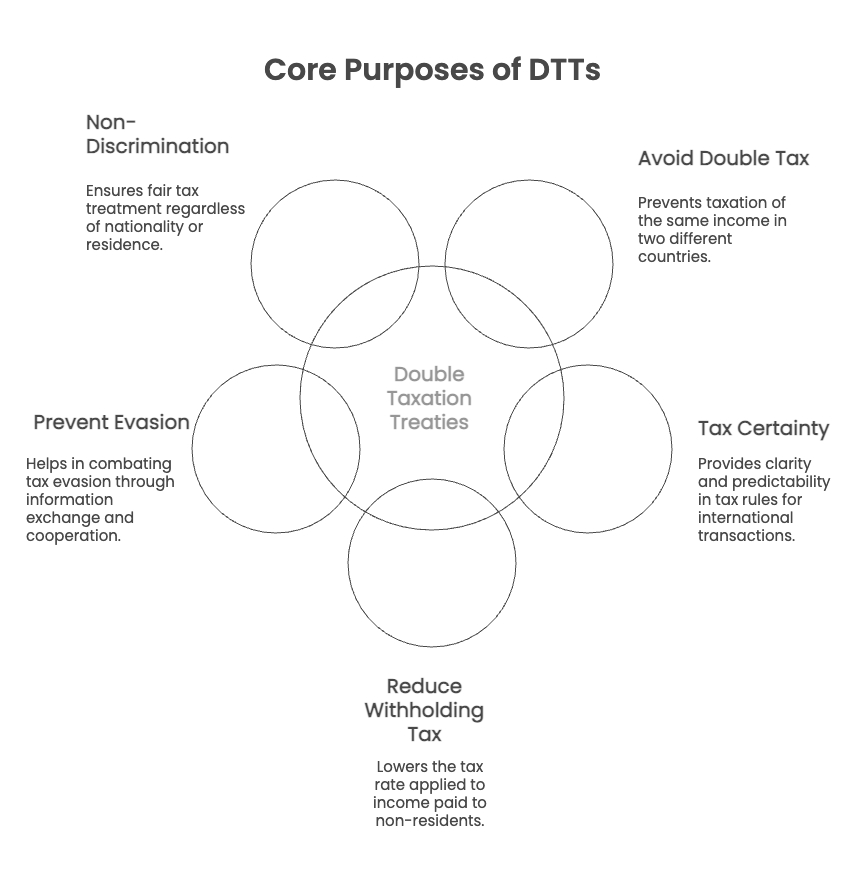

A Double Taxation Treaty is a bilateral agreement concluded between two sovereign states (Contracting States) designed primarily to:

- Prevent Double Taxation: Allocate taxing rights between the two countries to ensure that income earned by a resident of one country from sources in the other country is not taxed by both jurisdictions, or if it is, that relief is provided.

- Provide Tax Certainty: Offer clarity and predictability on how various types of income (e.g., dividends, interest, royalties, business profits) will be taxed, fostering a more stable environment for cross-border trade and investment.

- Reduce or Eliminate Withholding Taxes: DTTs often provide for reduced rates (or even exemption) of withholding taxes on payments like dividends, interest, and royalties flowing between the two countries.

- Prevent Fiscal Evasion: Include provisions for the exchange of tax information between the tax authorities of the two countries to combat tax avoidance and evasion.

- Promote Non-Discrimination: Ensure that nationals or residents of one state are not treated less favourably in the other state than that other state’s own nationals or residents in similar circumstances.

Most DTTs are based on model conventions, primarily the OECD Model Tax Convention on Income and on Capital, which provides a common framework and interpretation guidelines. Malta’s treaties largely follow this model.

How Malta’s DTTs Work in Practice to Eliminate Double Taxation

DTTs employ several methods to achieve their primary goal of eliminating or mitigating double taxation on income that could potentially be taxed in both Malta and the treaty partner country:

1. Exemption Method:

- Under this method, the country where the taxpayer is resident exempts the income derived from the other treaty country from its own tax.

- Example: If a Maltese company receives profits from a branch (Permanent Establishment – PE) in a treaty partner country, and the DTT stipulates the exemption method, Malta might exempt those branch profits from Maltese tax, as they have already been (or will be) taxed in the country where the branch is located.

2. Credit Method:

- This is the more common method found in Malta’s DTTs. The country where the taxpayer is resident taxes the income from the other treaty country but provides a credit for the tax already paid in that other (source) country.

- The credit is typically limited to the amount of tax that the residence country would have charged on that same income (ordinary credit).

- Example: A Maltese company receives interest income from a treaty partner country, and that country has levied a 10% withholding tax on the interest. When Malta taxes this interest income (as part of the company’s worldwide income), it will allow a credit for the 10% tax already paid in the source country against the Maltese tax due on that interest. This ensures the interest isn’t fully taxed twice. This mechanism is vital for businesses that have completed their Malta company registration and are trading internationally.

3. Allocation of Taxing Rights (Distributive Rules):

- DTTs contain specific articles that allocate or share the right to tax different types of income between the country of source (where the income arises) and the country of residence of the recipient.

- Business Profits (Article 7 of OECD Model): Generally, the profits of an enterprise of one state are taxable only in that state unless the enterprise carries on business in the other state through a Permanent Establishment (PE) situated therein. If it does, the profits attributable to that PE may be taxed in the PE state. Malta’s DTTs define what constitutes a PE (e.g., a fixed place of business like an office, branch, factory).

- Dividends (Article 10): May allow the source country to impose a limited withholding tax (e.g., 5%, 10%, 15%) on dividends paid to a resident of the other state. The residence country will also typically tax the dividend but provide a credit for the withholding tax paid. (Note: Malta itself generally does not levy withholding tax on outbound dividends paid to non-residents, irrespective of a treaty.)

- Interest (Article 11): Often provides for a reduced withholding tax rate (e.g., 0%, 5%, 10%) in the source country on interest paid to a resident of the other state.

- Royalties (Article 12): Similar to interest, usually provides for reduced (or zero) withholding tax rates in the source country on royalty payments.

- Capital Gains (Article 13): Allocates taxing rights for gains from the disposal of different types of assets (e.g., immovable property typically taxed where located; gains from shares often taxed in the seller’s country of residence, with exceptions).

- Income from Immovable Property (Article 6): Typically taxed in the country where the property is situated.

By clearly defining these taxing rights, DTTs prevent both countries from fully taxing the same income without relief.

Key Benefits of Malta’s DTT Network for Your Business

Leveraging Malta’s extensive network of DTTs can bring tangible financial and strategic advantages to your Maltese company:

- Reduced Withholding Taxes on Incoming Payments: If your Maltese company receives dividends, interest, or royalties from a company resident in a treaty partner country, the DTT can significantly reduce or eliminate the withholding tax that the source country would otherwise impose on such payments. This directly increases the net amount of income received by your Maltese company.

- Practical Example: If your Malta company licenses intellectual property to a company in Treaty Country X, and Country X normally imposes a 25% withholding tax on royalties paid to non-residents, a DTT might reduce this to 5% or 0%, leading to substantial savings.

- Prevention of Double Taxation on Foreign Branch Profits: If your Maltese company operates a branch (Permanent Establishment) in a treaty country, the DTT will provide a mechanism (exemption or credit) to ensure the profits of that branch are not fully taxed in both jurisdictions.

- Certainty on Tax Treatment of Cross-Border Transactions: DTTs provide clear rules, reducing ambiguity and allowing for more predictable tax planning for international operations. This stability is crucial for investment decisions.

- Facilitation of Repatriation of Profits: While Malta itself generally doesn’t impose withholding tax on outbound dividends, the DTTs can be relevant for the shareholders of the Maltese company if their country of residence taxes foreign dividend income. The treaty might influence how their home country taxes the Maltese dividend.

- Enhanced Credibility: Operating within a network of internationally recognized tax treaties can enhance the perceived legitimacy and stability of your Maltese operations, particularly when dealing with international partners or financial institutions.

- Mutual Agreement Procedure (MAP): DTTs typically include a MAP article, which allows taxpayers to request assistance from the competent authorities of their country if they believe they are being taxed not in accordance with the provisions of the treaty. This provides a dispute resolution mechanism.

These benefits are integral to using Malta as an efficient hub for international business, a key consideration from the initial stages of Malta business setup.

Accessing Treaty Benefits: Key Requirements

Simply having a Maltese company and a DTT in place with another country doesn’t automatically guarantee benefits. Certain conditions generally need to be met:

- Tax Residency: The entity seeking to claim treaty benefits (e.g., your Maltese company, or a foreign company paying your Maltese company) must be a tax resident of one of the Contracting States as defined by the relevant DTT. A Certificate of Tax Residence from the Maltese tax authorities is often required to prove Maltese residency to a foreign tax authority.

- Beneficial Ownership: For benefits related to dividends, interest, and royalties, the recipient must typically be the beneficial owner of that income. This means they must have the right to use and enjoy the income, not merely acting as a nominee or conduit for someone else.

- Substance & Principal Purpose Test (PPT): This is increasingly critical. Modern DTTs (especially those updated post-BEPS) include a Principal Purpose Test. Treaty benefits may be denied if obtaining that benefit was one of the principal purposes of an arrangement or transaction, unless granting the benefit would be in accordance with the object and purpose of the relevant treaty provisions. This ties directly into demonstrating genuine economic substance in Malta. A Maltese company that is merely a “shell” or “conduit” may be denied treaty benefits.

- Specific Article Requirements: Each article of a DTT (e.g., for dividends, interest) will have its own specific conditions that must be met.

Actionable Tip: When planning cross-border transactions, always review the specific DTT between Malta and the relevant partner country. Do not assume all treaties are identical. The wording and rates can vary. The Maltese Commissioner for Revenue’s website provides a list of active DTTs.

The Role of Your Corporate Service Provider and Tax Advisor

Navigating the complexities of DTTs, determining eligibility for benefits, and making formal claims (e.g., applying for reduced withholding tax in a foreign country) often requires professional expertise.

At Contact Advisory Services Ltd., while we are not tax advisors ourselves, we play a crucial role by:

- Structuring for Treaty Access: During the Malta company incorporation phase, we consider with you how your intended international operations might interact with Malta’s DTT network.

- Facilitating Tax Residency Certificates: We can assist in obtaining Certificates of Tax Residence from the Maltese tax authorities, which are often required by foreign counterparties to grant treaty benefits.

- Liaising with Tax Advisors: We work closely with your chosen Maltese and international tax advisors to ensure that your company structure and transactions are optimized to legitimately access available treaty benefits. Tax advisors are essential for interpreting specific treaty articles and advising on compliance with PPT and substance requirements.

- Ensuring Proper Corporate Governance: Maintaining good corporate governance and clear documentation of commercial rationale for transactions helps support claims for treaty benefits.

Properly leveraging Malta’s DTT network is a collaborative effort between your business, your corporate service provider, and specialist tax advisors.

Conclusion: Malta’s DTTs – A Vital Tool for International Tax Efficiency

Malta’s extensive network of over 70 Double Taxation Treaties is a cornerstone of its attractiveness as an international business hub. These bilateral agreements provide a vital framework for preventing double taxation on cross-border income, reducing withholding taxes on dividends, interest, and royalties, and offering greater tax certainty for businesses operating internationally through a Maltese company.

By clearly allocating taxing rights and providing mechanisms for relief (such as the credit method), Malta’s DTTs help ensure that profits generated from international activities are not unduly eroded by being taxed in multiple jurisdictions. This directly enhances the financial efficiency and competitiveness of Maltese companies engaged in global trade and investment.

However, accessing these benefits requires careful attention to residency requirements, beneficial ownership conditions, and the increasingly important principle of demonstrating genuine economic substance and a principal purpose aligned with the treaty’s objectives. Navigating these complexities and the specific provisions of each individual treaty underscores the need for expert corporate structuring and ongoing tax advice.

By strategically considering Malta’s DTT network from the initial stages of Malta company formation, businesses can lay a strong foundation for efficient and compliant international operations.

Are you planning international business activities through a Maltese company and want to understand how Malta’s Double Taxation Treaties can benefit you?

Contact Contact Advisory Services Ltd. for expert guidance and to be connected with specialist tax advisors:

Email: info@contact.com.mt