For international entrepreneurs and corporate groups seeking an optimized, onshore European headquarters, Malta remains one of the most attractive jurisdictions in the EU. At the heart of this appeal is its robust, EU-approved full imputation system. While the island nation levies a headline corporate tax rate of 35%, its unique shareholder refund mechanism legally slashes the final, effective tax exposure down to just 5% for trading income.

However, capturing this massive fiscal advantage requires a precise understanding of the underlying compliance mechanics, corporate architecture, and timeline realities. Missteps in your timing or corporate structure can lead to cash flow bottlenecks or unintended tax consequences in your home country. This comprehensive guide details the exact step-by-step process of navigating the Malta company tax refund system, structuring your corporate layout for maximum protection, and setting realistic expectations for your liquidity timelines.

How long does it take to get a tax refund in Malta?

When utilizing electronic filing through an authorized tax practitioner, the Malta Tax and Customs Administration (MTCA) typically processes and issues the 6/7ths corporate tax refund within 14 working days to a few weeks from the date of correct submission, provided that all company tax payments, statutory returns, and shareholder refund claims are flawlessly aligned.

The Underlying Mechanism: Understanding Malta’s Full Imputation System

To master the timeline, you must first understand the legal foundation. Malta does not operate as a traditional “tax haven” with opaque tax practices or zero-tax structures. Instead, it utilizes an open, fully transparent Full Imputation System that has been actively scrutinized and sanctioned by both the European Union and the OECD.

Under a full imputation system, profits generated by a Maltese company are taxed at the standard corporate rate of 35%. However, when those profits are distributed as a dividend to shareholders, the tax paid by the company is “imputed” directly to the shareholder. Because the corporate tax already covers the tax liability on that income, shareholders receive a tax credit representing the 35% tax already paid by the company, ensuring that the exact same profit is never taxed twice.

To further incentivize international investment, Malta allows shareholders to claim a substantial refund on the corporate tax paid by the distributing company. For active trading income, this refund amounts to 6/7ths of the corporate tax.

The Mathematics of the 6/7ths Refund

To see how this operates dynamically, consider a company that generates active trading income:

| Financial Metric | Amount / Calculation |

| Net Taxable Trading Profit | €100,000 |

| Malta Corporate Tax (35%) | €35,000 |

| Profit Available for Distribution (Dividend) | €65,000 |

| Shareholder Tax Refund Claim (6/7ths of €35,000) | €30,000 |

| Final Net Tax Retained in Malta | €5,000 (Effective 5%) |

International Tax Compliance Note: Following the global rollout of the OECD’s Pillar Two framework, Malta continues to fully preserve its 5% effective corporate tax rate for small and medium-sized enterprises (SMEs) and corporate groups with a consolidated annual revenue below €750 million. For international startups, mid-tier trading companies, and scaling family offices, Malta’s traditional refund system remains completely unaffected by the 15% global minimum tax directives.

While the mathematical outcome is highly appealing, the execution requires navigating a multi-stage corporate and administrative timeline. Ensuring that your entity is correctly registered from day one is critical; when initiating your Malta company incorporation process, setting up your tax accounts correctly prevents future friction with the revenue authorities.

The Step-by-Step Corporate Tax & Refund Timeline

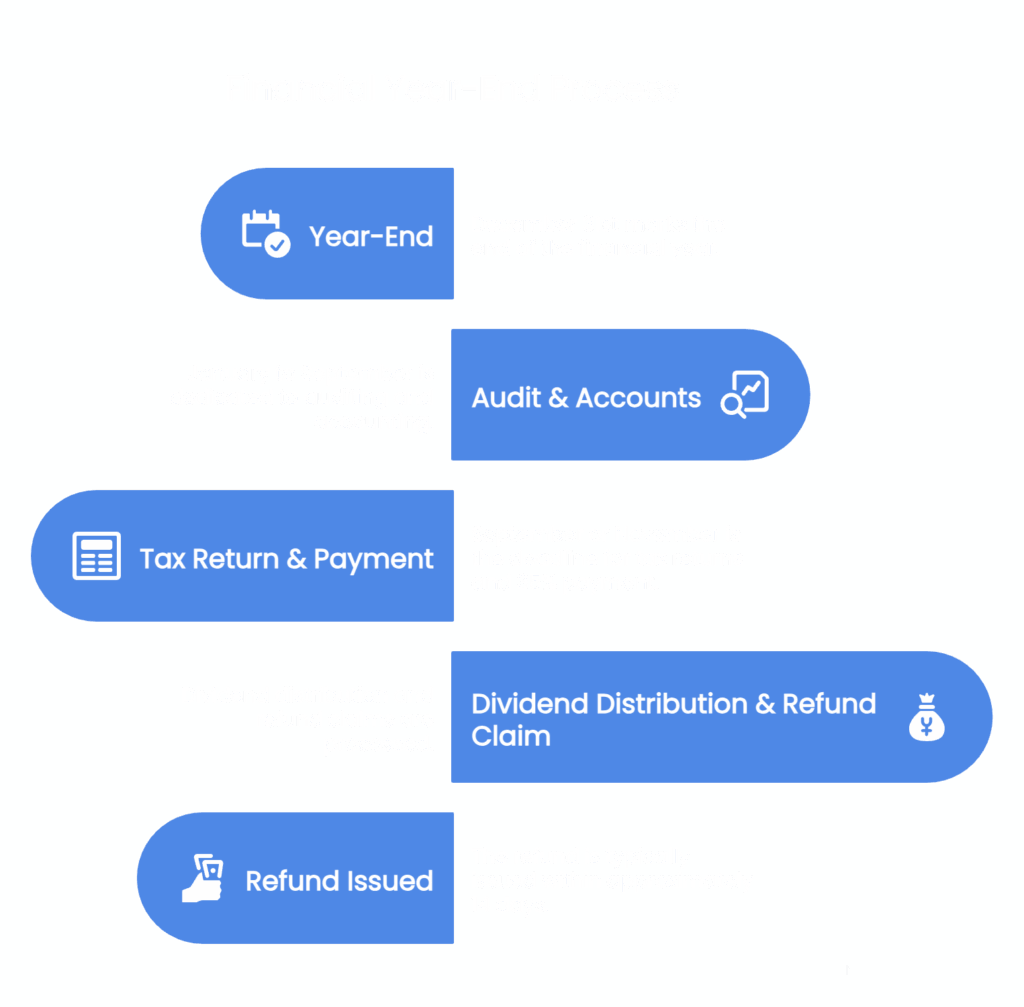

The tax refund process does not happen overnight. It follows a strict chronological loop driven by the company’s financial year-end. For illustrative purposes, let us assume a company utilizes a standard calendar year-end of December 31st.

[Year-End: Dec 31] ➔ [Audit & Accounts: Jan-Sept] ➔ [Tax Return & 35% Payment: Sept/Nov] ➔ [Dividend Distribution & Refund Claim] ➔ [Refund Issued: ~14 Days]

Step 1: Closing the Financial Year and Preparing Accounts

- Timeline: January to June (following the basis year)

- Action: The company closes its books on December 31st. A certified public auditor in Malta must audit the financial statements.

During this phase, profits must be properly allocated to their respective tax accounts. In Malta, company profits are segmented into five distinct tax accounts:

- MTA (Malta Taxed Account): Used for allocating trading profits; securing the 6/7ths refund depends entirely on accurate allocation here or to the FIA.

- FIA (Foreign Income Account): Used for allocating foreign-sourced income; securing the 6/7ths refund depends entirely on accurate allocation here or to the MTA.

- IPA (Immovable Property Account): Used for profits derived from immovable property in Malta.

- UA (Untaxed Account): Used for allocating remaining untaxed profits.

- FTA (Final Tax Account): Used for profits subject to a final withholding tax.

Step 2: Approval and MBR Filing

- Timeline: Within 10 months of the financial year-end (typically by October 31st for private companies)

- Action: Action: The directors and shareholders formally approve the audited financial statements, which are then submitted to the Malta Business Registry (MBR) within 42 days of approval.

Step 3: Submission of Corporate Tax Returns and Upfront Payment

- Timeline: 9 months after year-end for manual filings (September 30th) or up to 11 months for authorized electronic filings (typically late November). Crucially, the tax payment must still be made by September 30th.

- Action: The Maltese company submits its corporate income tax return (Form T10) to the Malta Tax and Customs Administration Form T10. Concurrently, the company must remit the full 35% corporate tax upfront. The refund process cannot begin until the tax liability of the operating company is completely settled.

Step 4: The Dividend Resolution and Shareholder Registration

- Timeline: Immediately following or concurrent with the tax return submission

- Action: The directors pass a resolution to distribute the remaining 65% of profits as a dividend to the registered shareholders. Alongside the dividend distribution, the company issues a dividend certificate detailing the gross dividend, the tax credit (the 35% already paid), and the net dividend.

Step 5: Submission of the Shareholder Tax Refund Claim

- Timeline: Initiated immediately after the dividend distribution

- Action: The shareholder (or their authorized tax practitioner) submits the formal refund claim (Form UA) to the Malta Tax and Customs Administration Form UA. This application explicitly references the dividend certificate and requests the 6/7ths refund of the underlying tax paid.

Step 6: Verification and Refund Disbursement

- Timeline: Typically 14 working days to a few weeks from electronic submission

- Action: The Malta Tax and Customs Administration reviews the application against the operating company’s paid tax records. If the accounts match perfectly, the refund is approved and wired directly into the shareholder’s designated bank account in the currency in which the operating company paid its tax (minimizing foreign exchange exposure).

Structural Necessity: The Holding Company Setup

One of the most critical elements of a successful Maltese corporate setup is the architecture of ownership. If an international entrepreneur holds shares in a Maltese operating company directly as an individual, the tax refund will be paid straight into their personal bank account. For residents of countries with high personal income taxes or aggressive Controlled Foreign Corporation (CFC) laws, this direct payout can trigger an immediate, highly punitive personal tax event at home, completely erasing the benefits of the Maltese system.

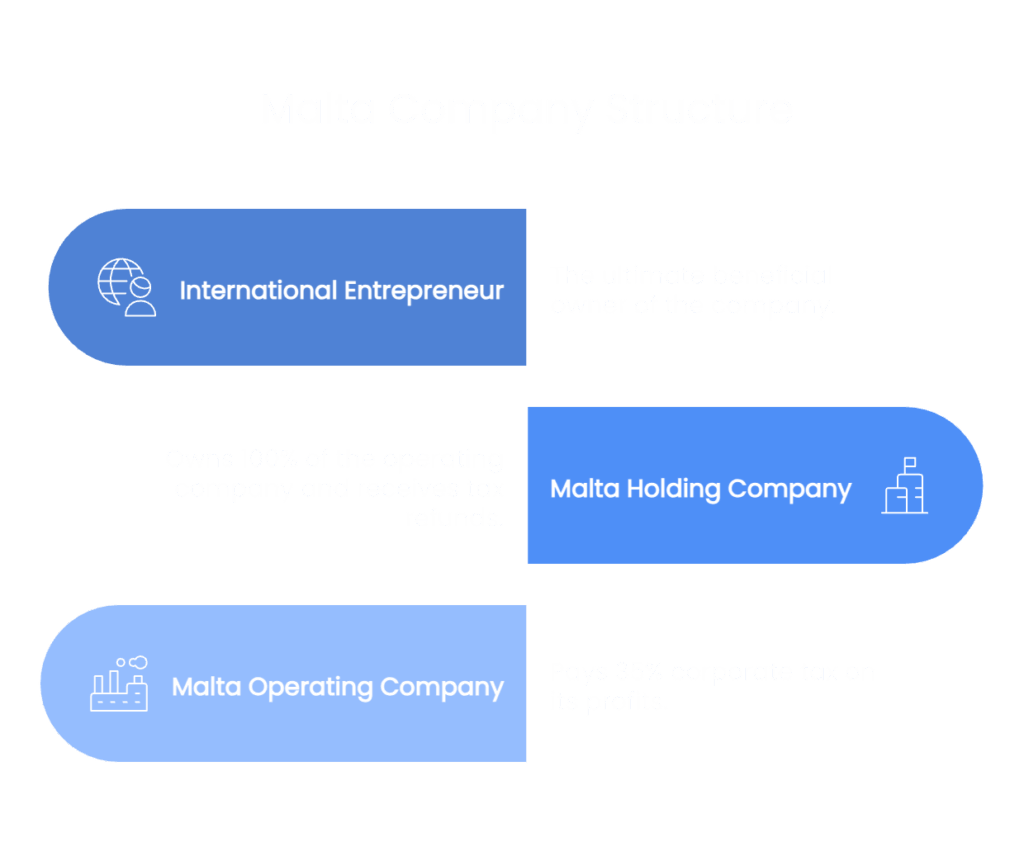

To mitigate this, international tax planners almost universally utilize a Two-Tier Architecture:

[ International Entrepreneur / Ultimate Beneficial Owner ]

│

▼

[ Malta Holding Company ]

│ ▲

(100% Shareholding) │ │ (6/7ths Refund Sent Here)

▼ │

[ Malta Operating Company ]

│

▼

(Pays 35% Corporate Tax)

(Visual representation of the corporate layout)(Visual representation of the corporate layout)

Why the Holding Company Structuring is Essential

- Tax Deferral & Consolidation: When the operating company pays its 35% tax and distributes a dividend, the dividend and the subsequent 6/7ths tax refund flow cleanly into the Malta Holding Company. Under Maltese tax law, dividends and tax refunds moving between a Maltese operating company and a Maltese holding company are completely exempt from further taxation.

- Avoiding Immediate Home-Country Taxation: The funds sit safely at the holding company level in the EU. As long as the cash remains within the holding structure and is not distributed onward to the individual entrepreneur, it does not trigger personal dividend tax in the owner’s country of residence (subject to local CFC and tax residency rules).

- Reinvestment Vehicle: The holding company can act as an internal corporate treasury. The accumulated cash (reflecting an effective 5% tax rate) can be deployed directly from the holding company into new global investments, real estate, software development, or subsidiary expansions without ever being diminished by high personal income tax rates.

Setting up this specific structure properly from the start is paramount for international tax efficiency. Entrepreneurs looking to establish this framework seamlessly should evaluate their options during their initial Malta business setup phase.

Key Pitfalls That Can Delay Your Refund

While the Malta Tax and Customs Administration aims for a swift 14-day electronic turnaround, certain procedural errors can stall refunds for months. To protect your company’s cash flow, avoid these common operational pitfalls:

1. Incurring Tax Mismatches and Delinquencies

If the operating company has outstanding balances, missing VAT returns, unpaid employer taxes (FSS/PE), or penalties from previous years, the Malta Tax and Customs Administration will halt the shareholder’s refund. The system requires complete compliance across all tax departments before any capital is released.

2. Incorrect Allocation of Tax Accounts

If your accountant incorrectly allocates trading profits to the Untaxed Account or miscalculates passive interest (which triggers a 5/7ths refund rather than a 6/7ths refund), the tax return will be flagged. Resolving an administrative audit or query can extend the refund timeline significantly.

3. Banking and KYC Hurdles

The refund must be paid to the registered shareholder’s bank account. If the holding company’s bank account is frozen, undergoing routine KYC reviews, or incapable of accepting transfers in the specific currency of the refund, the funds will bounce back to the central bank, causing severe administrative delays.

The Alternative Strategy: The Malta Fiscal Unit (Tax Consolidation)

For corporate groups that find the process of paying 35% upfront and waiting for a 6/7ths refund administratively cumbersome, Malta introduced an evolved framework: The Malta Fiscal Unit regulations.

Under this system, a parent company and its qualifying subsidiaries can elect to form a single fiscal unit for tax purposes. The primary advantage of this consolidation is the elimination of the traditional cash flow gap. Instead of the operating subsidiary paying 35% tax and the holding company waiting weeks for a 30% refund, the Fiscal Unit allows the group to calculate its net liability and pay the 5% effective tax directly to the revenue authorities in a single transaction.

While highly efficient for cash flow, forming a Fiscal Unit requires a higher tier of ongoing administrative maintenance, including consolidated audited accounts and strict ownership requirements (the parent must hold at least 95% of the subsidiary). For many scaling startups and agile entrepreneurs, the traditional two-tier refund system remains the preferred path due to its lower operational overhead.

Executive Summary Checklist for Entrepreneurs

To ensure your Malta company tax refund process operates like clockwork, adhere to this strategic operational checklist:

- Establish a Two-Tier Structure: Set up both a Malta Holding Company and a Malta Operating Company to receive refunds safely.

- Partner with a Local Auditor: Ensure a certified Maltese auditor reviews and signs off on your financial statements by mid-year.

- Accurately Allocate Profits: Confirm that active trading income is explicitly funneled to the Malta Taxed Account (MTA).

- Settle the 35% Liability Promptly: Ensure your operating entity remits its full corporate tax payment by September 30th.

- Leverage Electronic Tax Filing: Always file tax returns and refund applications electronically through an authorized practitioner to secure the accelerated 14-day processing window.

- Maintain Corporate Health: Keep all peripheral filings, including MBR annual returns and VAT submissions, entirely up to date.

Frequently Asked Questions (FAQs)

Can an individual entrepreneur claim the Malta tax refund directly?

Yes, but if an international entrepreneur holds shares directly as an individual, the refund is paid straight into their personal bank account. For residents in countries with high personal income taxes or aggressive CFC laws, this can trigger immediate, punitive personal tax events at home. This is why a two-tier holding structure is almost universally recommended.

What happens if the operating company has outstanding balances in other tax departments?

If the operating company has outstanding balances, missing VAT returns, unpaid employer taxes (FSS/PE), or penalties from previous years, the MTCA will halt the shareholder’s refund until complete compliance across all departments is achieved.

Does the Malta Fiscal Unit eliminate the 35% upfront corporate tax payment?

Yes. Instead of the operating subsidiary paying 35% upfront and the holding company waiting weeks for a refund, the Fiscal Unit framework allows the consolidated group to pay the 5% effective tax directly to the revenue authorities in a single transaction.

What happens if trading profits are incorrectly allocated to the Untaxed Account?

Incorrectly allocating trading profits to the Untaxed Account or miscalculating passive interest (which triggers a 5/7ths refund instead of a 6/7ths refund) will cause the tax return to be flagged, resulting in administrative audits or queries that significantly extend the refund timeline.

Ready to Streamline Your Maltese Corporate Structure?

Navigating cross-border corporate taxation requires precision, deep localized expertise, and proactive compliance management. Setting up a highly efficient corporate structure in Malta ensures your business retains its hard-earned capital while remaining fully compliant with EU regulations.

Whether you are looking to launch a brand-new entity, establish a robust holding structure, or transition to a direct 5% effective tax rate via a Fiscal Unit, professional guidance makes all the difference. Get in touch with our corporate structuring specialists today to execute your corporate entity launch in Malta with absolute confidence, optimized cash flow, and complete regulatory compliance.